The Trump administration has launched an aggressive effort to dismantle the Consumer Financial Protection Bureau (CFPB), a government agency established in the aftermath of the 2008 financial crisis to protect consumers from fraud, predatory lending, and other deceptive financial practices. This move has ignited a fierce debate over the role of government in regulating financial markets, the consequences of eliminating consumer protections, and the potential conflicts of interest involved in the administration’s actions.

The Birth of the CFPB: A Response to Economic Collapse

The CFPB was created as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act, signed into law by President Barack Obama in 2010. The Great Recession, which followed the subprime mortgage crisis, devastated millions of Americans, wiping out nearly $8 trillion in stock market value and $6 trillion in home equity. Many families lost their homes due to misleading loan agreements and predatory banking practices. The CFPB was designed to prevent such crises from happening again by holding financial institutions accountable and ensuring consumers had access to fair and transparent financial products.

One of the CFPB’s strongest supporters is Senator Elizabeth Warren, who originally proposed the idea for the agency while working as a Harvard Law professor. “If you have a bank account, credit card, mortgage, or student loan, this is code red. I am ringing the alarm bell,” Warren warned. “Elon Musk and the guy who wrote Project 2025, Russ Vought, are trying to kill the Consumer Financial Protection Bureau. If they succeed, CEOs and Wall Street will once again be free to trick, trap and cheat you.”

What Does the CFPB Do?

Since its creation, the CFPB has enforced regulations that prevent financial institutions from engaging in deceptive or exploitative practices. The agency has secured $20 billion in relief for consumers by reducing loan balances, erasing debt, and issuing refunds to people harmed by fraudulent business practices. Some of its notable actions include:

- Penalizing banks and financial firms, including Wells Fargo, for opening fake accounts without customer consent.

- Imposing $5 billion in civil monetary penalties against companies that violated consumer protection laws.

- Banning excessive credit card late fees (though a federal judge blocked this rule in 2024).

- Tightening regulations on “Buy Now, Pay Later” services to prevent hidden fees and financial traps.

- Banning medical debt from appearing on consumer credit reports.

- Protecting military service members from illegal loans.

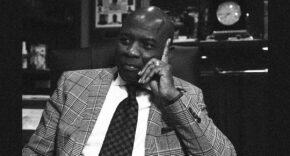

Former CFPB Director Rohit Chopra, who was recently fired by President Trump, described the agency’s mission clearly: “It’s a law enforcement agency. It takes big financial institutions to court who cheat consumers, whether it’s a credit reporting agency, or a large bank or a credit card giant. The CFPB has been recovering billions of dollars for consumers who were wronged.”

Trump’s Plan to Weaken the CFPB

On February 8, the Trump administration took a drastic step by ordering the CFPB to halt most of its operations. Acting director Russell Vought, a longtime critic of the agency, immediately laid off dozens of employees and froze ongoing investigations. He also canceled $100 million in contracts that allowed the CFPB to process consumer complaints, oversee financial regulations, and litigate against companies violating consumer protection laws.

Trump has been clear about his stance on the agency. “That was a very important thing to get rid of,” he told reporters. When asked if he intended to shut down the CFPB, he responded, “I would say, yeah, because we’re trying to get rid of waste, fraud, and abuse.”

Elon Musk, now leading Trump’s cost-cutting efforts through the Department of Government Efficiency, echoed this sentiment in a February 7 post on X, formerly Twitter, stating, “CFPB RIP 🪦.”

What Will Be Cut?

If Trump succeeds in dismantling the CFPB, several critical consumer protections will be lost, including:

- Credit Card Late Fee Caps: The CFPB’s rule capping most credit card late fees at $8, down from $32, is likely to be overturned.

- Overdraft Fee Limits: The agency had set a cap of $5 on overdraft fees, but banks are now free to raise these costs.

- Medical Debt Protections: Without the CFPB, medical debt could once again appear on credit reports, damaging consumers’ ability to secure loans or mortgages.

- Regulation of Tech-Based Payment Platforms: The CFPB had begun investigating the role of major tech companies in financial transactions, ensuring consumer protection against potential fraud and unfair practices.

Who is Fighting Back?

The push to dismantle the CFPB has sparked legal and political resistance. A federal employees’ union has sued the Trump administration, arguing that it lacks the authority to shut down a congressionally established agency. A U.S. District Judge has temporarily blocked further layoffs and destruction of CFPB records, preventing the administration from erasing critical data.

Senator Warren has led the charge against the CFPB shutdown. “Congress created the CFPB. Congress, and only Congress, has the power to end it. If they thought they could get enough votes, they could go get rid of the CFPB right now,” she stated. “So why don’t the Republicans do that? The answer is because it’s damn popular.”

Consumer advocacy groups, including the NAACP and the National Consumer Law Center, have also voiced strong opposition, warning that eliminating the CFPB would open the door for unchecked corporate abuse.

What’s Next?

Despite Trump’s aggressive moves, legal and legislative hurdles stand in the way of a complete shutdown. Congress, which created the CFPB, would need to pass new legislation to formally dissolve it. Meanwhile, courts are likely to scrutinize whether the administration’s actions are legal.

Financial analysts predict that while the CFPB’s power may be weakened, its core functions will likely survive in some form. “We expect to see the repeal of the credit card late fee, the overdraft late fee, and the open banking and credit bureau rules reversed by the courts,” said Jaret Seiberg, an analyst at TD Cowen Washington Research Group.

The battle over the CFPB is more than just a political fight—it’s a test of how much protection American consumers should have against corporate misconduct. Supporters argue that without the CFPB, financial institutions will revert to deceptive and exploitative practices that harm everyday people. Critics claim that the agency is redundant and overly burdensome on businesses.

With the legal battle ongoing and opposition mounting, Trump’s attempt to dismantle the CFPB may face significant resistance. For now, the fate of the agency—and the financial protections it provides to millions of Americans—hangs in the balance.