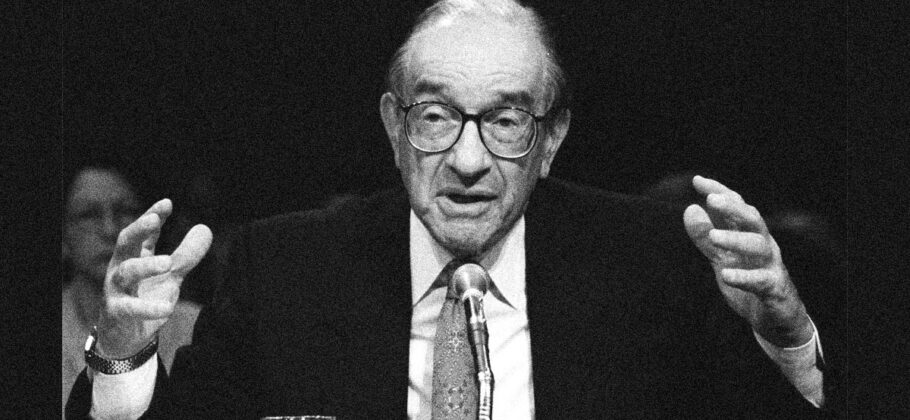

Alan Greenspan, one of the most influential economic policymakers in modern American history, died on June 22, 2026, at the age of 100. His wife, journalist Andrea Mitchell, announced that he died at his Washington home from complications of Parkinson’s disease. His passing marked the end of an era for a man who guided the U.S. economy through nearly two decades of extraordinary prosperity, financial shocks, and historic change.

Greenspan served as chairman of the Federal Reserve from August 1987 until January 2006, making him the second longest serving Fed chairman in history. Appointed by President Ronald Reagan, he was later reappointed by Presidents George H.W. Bush, Bill Clinton, and George W. Bush, an extraordinary show of bipartisan confidence in his leadership.

His wife described him as “a giant of a man who helped shape the U.S. economy for decades under presidents of both parties, but was always honest in acknowledging his mistakes.” She added, “He will be remembered for his brilliance and his kindness. Being his life partner was the joy of my life.”

The Chairman Who Became “The Maestro”

During Greenspan’s tenure, the United States experienced the second longest economic expansion in its history, a remarkable ten year period of uninterrupted growth from 1991 through 2001. Inflation remained surprisingly low despite rapid economic growth, unemployment fell, and the technology boom transformed the American economy.

His remarkable ability to interpret changing economic conditions earned him the nickname “The Maestro.” At one point he was widely considered the second most powerful person in Washington after the president because of the enormous influence the Federal Reserve wielded over the economy through interest rate policy.

Former Federal Reserve Chairman Jerome Powell later pointed to Greenspan’s judgment during the productivity boom of the 1990s as an example that “judgment can sometimes outperform technical models of the economy.” That willingness to rely on careful observation rather than rigid formulas remains influential among central bankers today.

His First Great Test: Black Monday

Greenspan’s defining moment arrived almost immediately after taking office.

Just two months into his chairmanship, on October 19, 1987, the stock market experienced Black Monday, when the Dow Jones Industrial Average plunged nearly 23 percent in a single day, the largest one day percentage decline in history.

The financial system appeared to be on the verge of panic.

Greenspan responded immediately. Before markets opened the following morning, the Federal Reserve pledged to provide liquidity to the financial system. The Fed injected cash into financial markets and lowered interest rates over the following months, restoring confidence before panic could spread throughout the economy.

His rapid intervention prevented what many economists feared could become another major recession. Today, his response is widely regarded as a textbook example of central bank crisis management.

That decisive action also established what later became known on Wall Street as the “Greenspan Put,” the expectation that the Federal Reserve would act aggressively to stabilize markets during periods of financial turmoil.

Guiding America Through Crisis After Crisis

The 1987 crash was only the beginning.

Throughout his nearly nineteen years leading the Federal Reserve, Greenspan successfully navigated numerous economic crises.

Among them were the 1990 to 1991 recession, the Asian financial crisis and Russian debt default of 1997 and 1998, the collapse of the dot com bubble in 2000, and the severe economic disruption following the terrorist attacks of September 11, 2001.

His willingness to provide liquidity quickly while carefully adjusting interest rates became a defining feature of his leadership.

Biographer Sebastian Mallaby also noted Greenspan’s remarkable political skills, writing that he became an exceptionally effective Washington operator who often persuaded presidents and cabinet officials to adopt policies he believed were in the nation’s best interest.

Economic Ideas That Continue to Influence the Fed

Many of Greenspan’s core monetary principles continue to shape Federal Reserve thinking today.

He believed inflation control was the foundation of long term economic prosperity. He also emphasized flexibility rather than rigid adherence to economic formulas, believing policymakers needed to respond to changing conditions as new information became available.

Greenspan generally preferred limited forward guidance, believing markets should not rely too heavily on detailed promises from the Federal Reserve about future policy actions. His famously cryptic communication style became known as “Fed speak.”

As Greenspan once joked:

“What I’ve learned at the Fed is a new language called ‘Fed speak.’ We learn to mumble with great incoherence.”

He later added:

“If I seem unduly clear to you, you must have misunderstood what I said.”

His emphasis on central bank credibility, inflation discipline, and careful judgment remains deeply embedded in Federal Reserve policymaking.

Kevin Warsh Revives the Greenspan Playbook

New Federal Reserve Chairman Kevin Warsh has openly embraced many of Greenspan’s governing principles.

During his swearing in ceremony, Warsh declared:

“I intend to fill the role of chairman with energy and purpose just the way Chairman Greenspan did, faithful to the mission and the very best traditions of the Fed.”

Warsh has already shortened Federal Reserve policy statements, eliminated much of the forward guidance that recent Fed leaders routinely provided, and placed renewed emphasis on controlling inflation.

Economists have noted the similarities.

Brian Wesbury, chief economist at First Trust, observed:

“Warsh’s philosophy on Fed communication seems to more closely resemble that of former long-time Chairman Alan Greenspan… Not Greenspan’s elegant and winding prose, but Greenspan’s unwillingness to hint strongly about what the Fed would do next.”

Warsh also faces economic conditions that closely resemble those Greenspan inherited in 1987, with core inflation running at nearly identical levels.

A Legacy Both Celebrated and Debated

Greenspan’s reputation suffered after the housing bubble burst in 2007 and the global financial crisis followed.

Critics argued that years of low interest rates and his strong belief in lightly regulated financial markets contributed to excessive risk taking by banks.

In a remarkable moment of public reflection before Congress in 2008, Greenspan acknowledged one of his greatest mistakes.

“Those of us who have looked to the self-interest of lending institutions to protect shareholders’ equity, myself included, are in a state of shocked disbelief.”

Yet many economists believe history should judge his career more broadly.

Former senior Federal Reserve official Stephen Oliner offered perhaps the most balanced assessment:

“I think the deification that came just before the financial crisis was never really deserved, and I think the lambasting that he took after he left was never fully deserved either.”

The Federal Reserve itself praised Greenspan’s enduring contributions, stating:

“He brought rigorous analytical discipline to monetary policymaking and helped establish the credibility that remains one of the Federal Reserve’s most important assets.”

An Enduring Figure in Economic History

Few individuals have shaped modern American economic policy as profoundly as Alan Greenspan.

For nearly two decades he guided the nation through market crashes, recessions, international financial contagions, technological revolutions, and national tragedy while overseeing one of the longest periods of sustained economic growth in U.S. history. Although later events sparked vigorous debate about some of his policies, his influence on central banking remains unmistakable.

With Kevin Warsh now reviving many of Greenspan’s communication style and inflation focused philosophy, the ideas of “The Maestro” appear likely to continue influencing Federal Reserve policy for years to come, ensuring that Alan Greenspan’s legacy extends well beyond his remarkable century of life.